Carvana Inches Closer to Bankruptcy

Plus a new feature from Temu and understanding VC fund math

Hi everyone, Turner back again with The Split 🍌. Welcome to all new subscribers and the 14,100+ readers tuning in every week!

Keep scrolling for my quick thoughts on Carvana, plus a new feature from Temu and a trick for founders to better understand how VC fund math works.

Carvana Inches Closer to Bankruptcy

The public markets valued online car dealer Carvana at over $50 billion last summer. So far this year its stock is down 98%, and down nearly 99% from its all-time highs. And now, its 10 largest creditors have reportedly made a pact to work together on a potential restructuring of over $4 billion in debt as it inches closer to bankruptcy

Why is Carvana's stock price down so much?

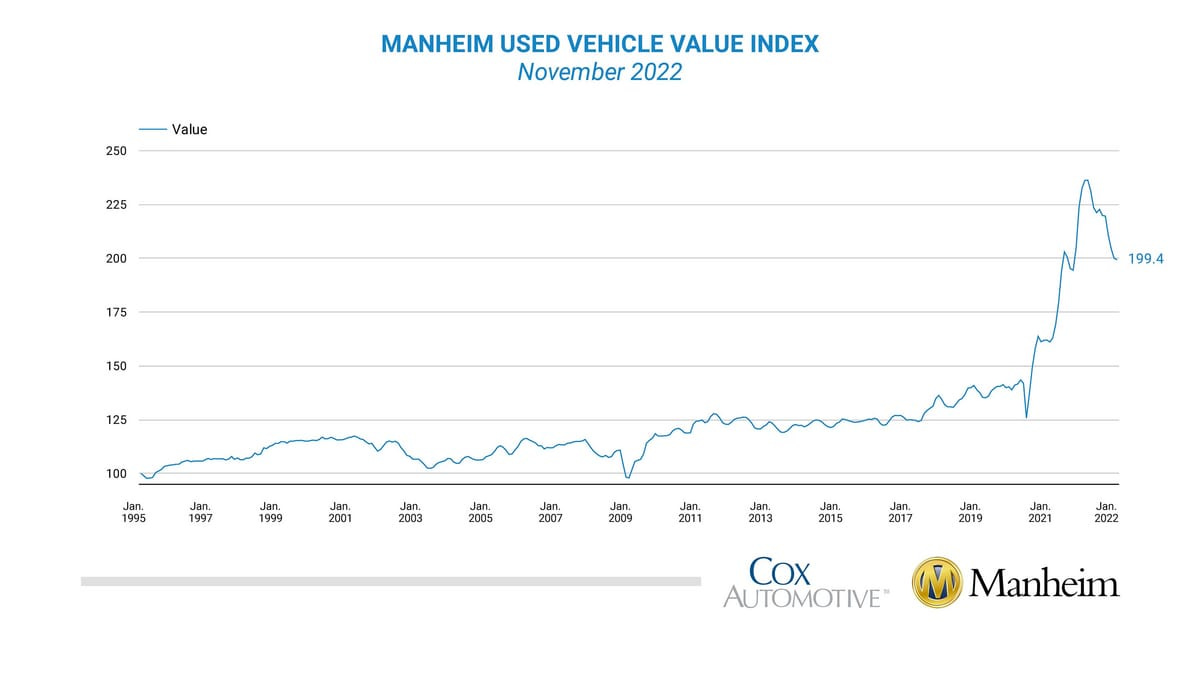

US used car prices reported their third consecutive month of declines in November, down 14.2% year-over-year. Prices are now down nearly 30% from all-time highs three months ago.

What's even more alarming is that many vehicles are ending their auction with ZERO bids. This means buyers didn't even want to pay the sellers initial list prices, hinting at further downside ahead (Shoutout to CarDealershiGuy for his consistent coverage of this).

In 2021, things were looking good for Carvana, at least in the summer (and looking back at full-year numbers). Revenue and Gross Profit per unit sold, essentially its profits on each sale not including any overhead costs, was trending up and even accelerated throughout the year. But when you compare it to used car prices nearly doubling in 2021, it was hard for the business not to look good.

At this point, a downward spiral in prices is a big deal for Carvana. Its financials reported to the SEC showed it took an average of 81 days to sell each vehicle it had in inventory. Three months of declining prices means that Carvana will soon be underwater on its $2.6 billion worth of inventory, if it isn't already. There is of course some nuance to this: the pace of sales to consumers has slowed, and the team is probably making decisions like slowing inventory purchases and favoring higher margin vehicles and upsells to offset some of this pressure.

Carvana's outlook is fairly straightforward from this perspective. Selling cars has low gross margins and requires significant working capital. Carvana financed much of its growth with debt, which worked great in 2021 when low interest rates and price inflation running rampant (due to supply chain constraints) made it hard to lose money. Now, it has $4 billion in debt with $2.6 billion in inventory that it can't make much money on and is declining in value.

With inflation reversing and higher interest rates making it harder for consumers to finance vehicle purchases. Carvana needs to figure out how to make money with much of its inventory potentially worth less than what it originally paid. In July I wrote about how it appeared to be accelerating its third party marketplace, which basically meant it was selling cars for other dealers. In November it reversed course, shutting down that product.

Its hard to know exactly where Carvana goes from here. But this reversal is why we invested in VINN in the summer of 2021 (more here). It provides a similar online experience to consumers while helping its dealer partners move their own inventory, similar to what Carvana attempted earlier this year.

Whether Carvana survives or not, the automotive market is one of the largest in the world. It makes up roughly 3% of US GDP and 20% of all consumer retail spending. And yet despite this, only 1% of sales currently happen online. With standardization across models being a requirement of the mass production that makes cars affordable for consumers, at Banana we think eventually a company will build enough consumer trust that enables the majority of cars to be bought sight unseen online.

Like what you're reading?

Subscribe to The Split for more every week.

🚀 Product Launches

Temu launches incentivized referrals: After spending the past month on top of the US app store, Temu is selling $1.5 million in Gross Merchandise Volume (GMV) per day. This is apparently below internal targets. It's now rumored to be launching a feature that offers shoppers discounts for each new customer referred, very similar to the strategy its parent company Pinduoduo used to become one of the largest retailers in China.

I've written about Temu three times (pre-launch, post-launch, and when hitting #3 overall), and up until now it didn't seem to leverage Pinduoduo's referral strategy. Possibly due to the slow start (in its own words) or maybe always part of the plan, discounted products for referring friends could be a hit with consumers tightening their wallets during a recession. More on the referrals from TechNode.

🔗 Links and Charts

VC's need $2b in exits per $50m in their fund: Assuming a VC buys 10% of a company, they need $200m in exit value to produce a 4x gross / 3x net fund (this assumes no dilution), which is probably good enough to be considered a successful fund by them and their investors (especially for a fund being invested in 2022). I'll save the more complicated math for Jason's post, but this a framework founders can use to understand what a VC might be looking for in each investment. More from Jason at SaaStr.

Live commerce increases conversion and improves brand differentiation: A light McKinsey report on live commerce drawing lessons from China. Apparel and fashion is by far the top use case, with beauty and fresh food also seeing success. Additionally, nearly half of Gen Z US consumers self-report social media has the most influence on their purchase decisions. More from McKinsey.

Tokyo aims to be the "most startup-friendly" city in the world: The Japanese government is aiming to invest ¥10 trillion ($72 billion) pear year into its startup ecosystem by 2027. It wants to increase the number of startups in Japan to 100,000, up 10x from today. The program would emulate Station F in Paris, home to nearly 1,000 startups and include tax benefits, public support, collaboration. More from the Japan Times.

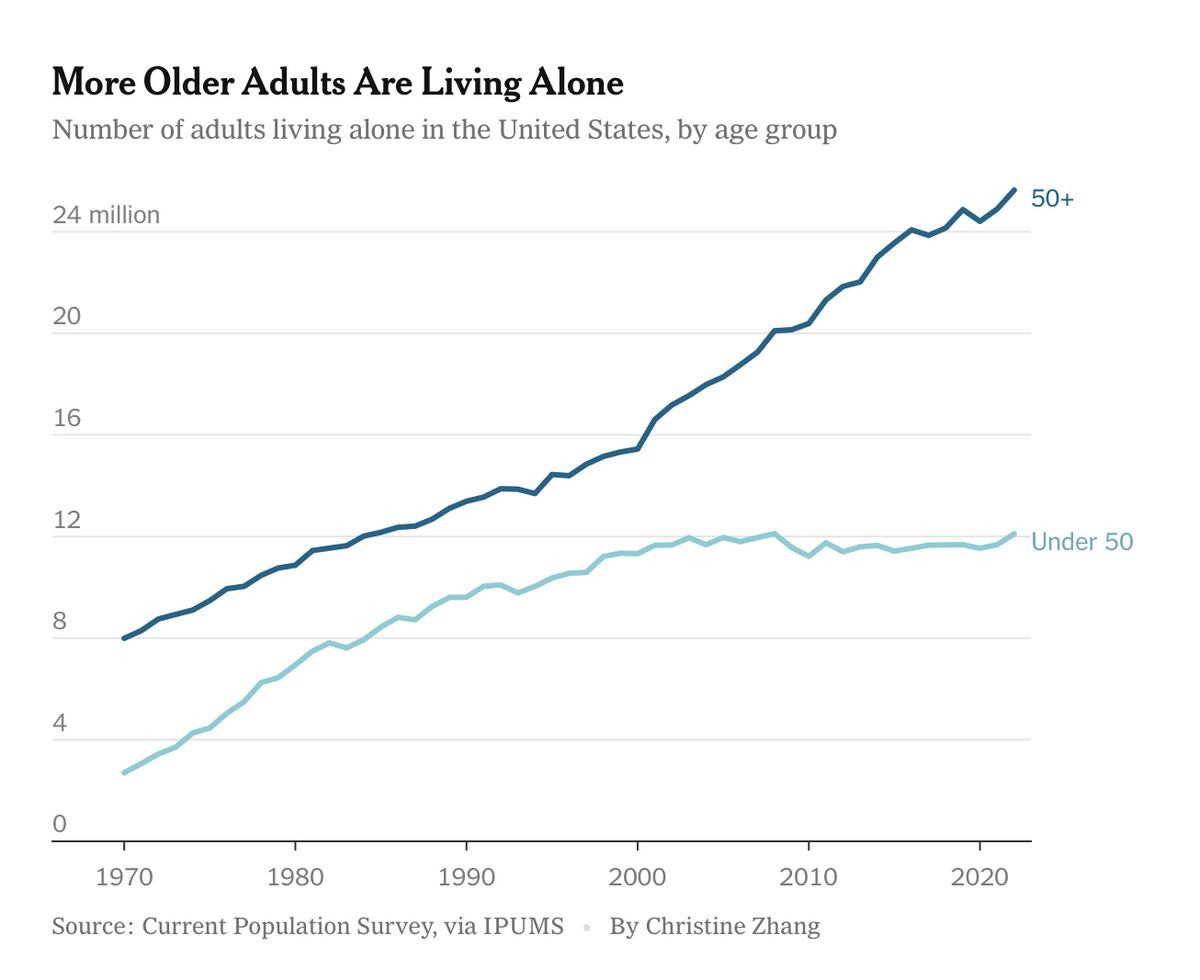

26 million Americans of age 50+ now live alone: This is up from 16 million in 2000. I haven't looked at what % of the 50+ population this is (it might actually be down!), but an interesting trend contrasted against our friendship recession. More from the NYT.

The Case for a Longer-Term Oil and Gas Bull Market: Perhaps controversial, a long read highlighting just how much of an impact oil and gas has on the global economy. More from Lyn Alden.

💼 Career Services

This Sunday we'll do Banana Talent Drop #8! The Banana Talent Collective now has 150+ candidates with experience from the companies below + many more (if you're at a Banana portfolio company, reach out for access).

Kelsey at Banana portfolio company Candor just made the most recent hire from the collective:

If you're starting to explore a new role or hiring and want a feed of pre-vetted candidates, click here to get started.

🍌 Monkey Business

🍌 The Split is brought to you by the team at Banana Capital. Read more about what we're up to at Banana here.

🤝 Interested in sponsorships with The Split? Inquire here.

🐝 And if you're thinking about starting your own newsletter, I can't recommend Beehiiv enough. Get started here.