Banana Capital Fund 2

Announcing our new $20 million fund

Hi everyone 👋 Turner back again with The Split. Big announcement today, so we’ll jump right in.

Announcing Banana Fund 2

After starting Banana Capital on January 1st of 2021 (read the Fund 1 launch here), I’m happy to announce our $20 million Banana Fund 2. The fund will make Pre-Seed and Seed investments averaging $500,000 (up to $1 million) into startups around the world.

The best part? After two years of sharing public updates on Twitter, old blog, and now here on The Split, we’re raising Fund 2 publicly. I’ll share more on why we can do this and how you can get involved.

If you’re interested in investing, indicate your interest here, and I’ll follow up within 24 hours.

Keep reading for a recap of Fund 1, what we’re building at Banana Capital, and more details on Fund 2.

Recapping Banana Fund 1

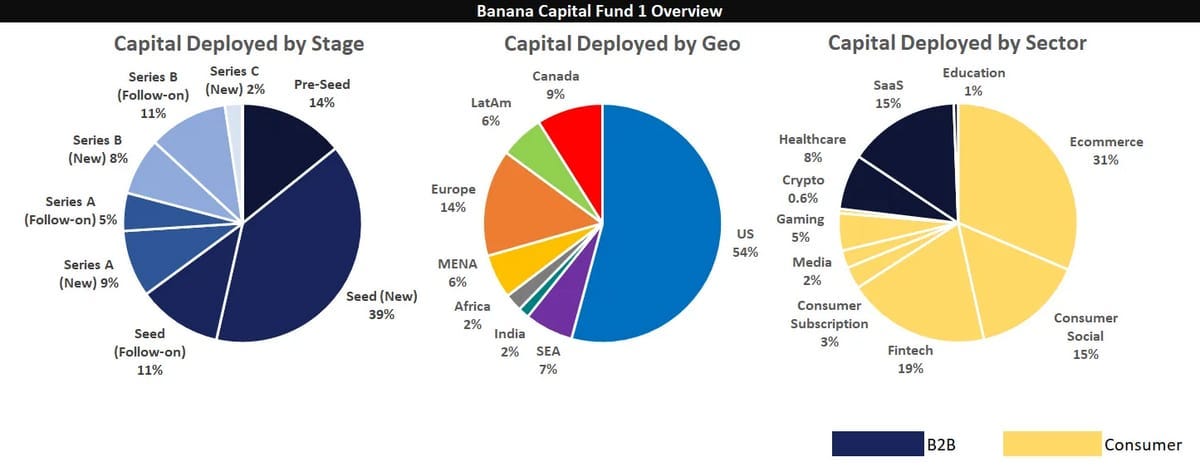

I started investing our $9.999 million Fund 1 in January of 2021, and man, it has been a crazy first two years. We increased our average check size by 4x from Q1 to Q4 of 2021, had a Seed investment sit on top of the App Store for months this past summer, and raised 11 SPVs. Seven followed-on to previous investments and four invested alongside our initial checks from Fund 1, up to $1.2 million or 7% of the company in one case.

Here’s what Fund 1 looks like today, with the caveat that most startups technically fall under multiple sector categories (and for some reason I’ve historically lumped Dev Tools into SaaS??):

We followed-on to some later stage companies that I had invested in pre-Banana (this was part of the plan). We also invested in a few new ones like Overtime (also part of the plan), which just signed a streaming deal with Amazon Prime and raised another round. If you remember when I announced Fund 1, I mentioned we’d make some public market and much later stage private investments. We ended up not doing either, and don’t plan to do so anytime soon.

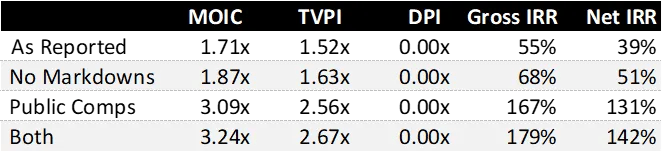

To end Q3 of 2022, Fund 1 reported a MOIC of 1.71x (gross returns), and a TVPI of 1.52x (returns net of all estimated fees and carried interest). This was based on valuations in the most recent round of financing and our own markdowns and write-offs.

Like everyone else, we unfortunately didn’t avoid all casualties. We marked down the valuation of some investments and wrote a few others down to zero. To give LPs (Limited Partners) more visibility and to compare with the performance of other funds, we also shared returns a) assuming no markdowns, b) using public market comps to value some now later stage companies, and c) both no markdowns and select public market comps. We don’t officially report these, but shared them to provide more context on the portfolio.

Banana Fund 2

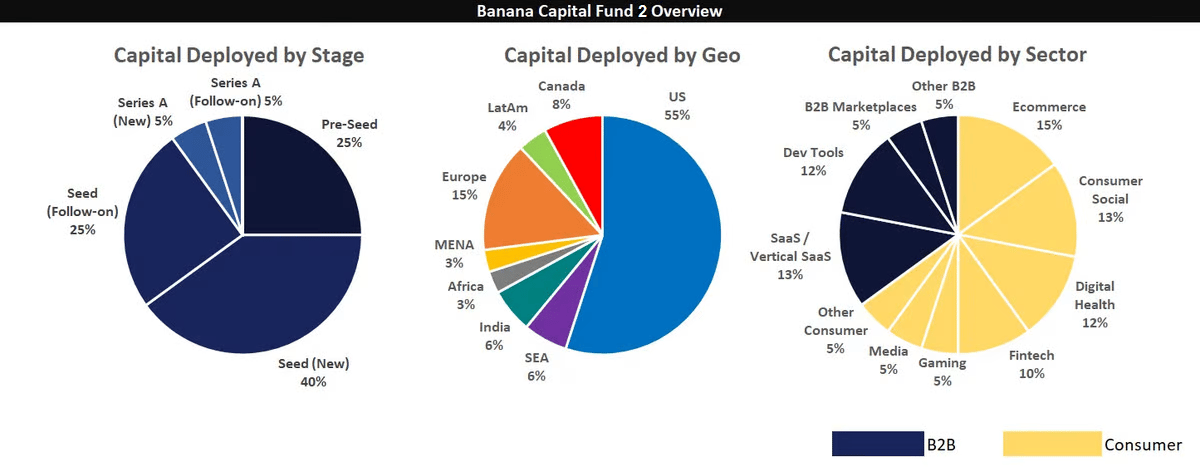

Fund 2 will be $20 million and make Pre-Seed and Seed investments globally. The fund will write initial checks averaging $500,000 (up to $1 million) with a target ownership of up to 5%. 50-75% of Fund 2 will be invested in North America, with the remaining across each of Europe, South and Southeast Asia, Latin America, MENA, and Africa.

Since I started investing in startups in Q4 of 2019, I’ve had four consumer Seed investments graduate to become unicorns based on previous funding rounds (which we can all agree may have been generous) and public comps, and we’re doubling down on investing in the best consumer-focused startups as early as possible.

Broadly speaking, we’re investing in exceptional founders solving big problems and making the world a better place. Sometimes this means building a 10x better product, and sometimes it means sustainably selling at a 10x lower cost.

We’ll keep investing in the themes below (+ others):

Broad shifts in consumer behaviors, like BeReal (Seed) and Bottomless

Commerce marketplaces and platforms, like Snackpass, JOKR (Seed), Facily (Seed), and VINN (Seed)

The changing entertainment landscape from media to gaming, like Overtime and Goals (Pre-Seed)

Improving access to healthcare, like NexHealth, Walnut, Millie (Seed) and Mindset (Pre-Seed)

Improving financial and housing accessibility, like Dwelling (Seed) and Extra (Seed)

Software that solves problems for customers, like Chainguard, Secureframe, and CreditBook (Seed)

Overall, Fund 2 largely continues what we’ve been doing in Fund 1. And if you’re a regular reader of this newsletter, you know all those bullet points above are the things we pay attention to around here.

If you’re building, investing in, or just curious about all these spaces, subscribe to follow along and reach out when it makes sense!

We’ve already made five core investments from Fund 2, and early co-investors include Sequoia, Founders Fund, and my old team at Afore Capital. Fund 2 will be more concentrated and skew earlier than Fund 1 - our average allocation earned for each core check has been at the high end of our target range at 4.3%.

We expect a fully invested Fund 2 portfolio to look something like this:

We’ll also keep raising SPVs to follow-on to breakout portfolio companies. Just like in Fund 1, we’ll loop in LPs that want additional exposure to each one. We’ll occasionally fill excess SPV allocation with non-Fund 2 LP checks from our syndicate on AngelList, which you can join here.

Meet the Team

You’ve probably noticed I keep mentioning “we”. Over the past two years, Banana has had a total of four employees. Arshia helped me the first summer after her freshman year at Stanford. Olivia joined full-time 14 months ago after investing in startups and venture funds at Silicon Valley Bank. And Wendy’s helping with The Split this semester while finishing up her MBA at Wharton.

We’re not specifically hiring at the moment, but I’m always meeting people who could add something new to the team.

Why Banana?

Why have founders been working with us? A few reasons:

Distribution: We help founders tell their story and acquire new customers. Back when I launched Fund 1, my friend Trung wrote about how I was “monetizing memes with venture capital”. Publicly, this happens on Twitter and The Split (this newsletter). Privately, this happens in the group chats.

Fundraising: We help our founders fundraise. Anytime they’re raising capital, we’re in the trenches with them. We commit early and help them put together rounds with the most relevant angels and funds. In three of our last five core investments, we’ve introduced the founders to their lead investor. And in the fourth and fifth, we were the largest investor in the round.

Recruiting: We’ve spent the past few months building the Banana Talent Collective. Recruiting is something we’ve been spending more time understanding exactly how we can help (it's hard!). The talent collective has since grown to a group of 150+ ambitious and smart individuals looking for jobs at fast growing tech companies, and nearly 50% of introduction requests between candidates and startups are accepted and lead to an initial call (if you’re reading this and looking for your next role at a breakout startup, apply as a candidate here). And helping founders tell their stories more broadly helps attract talent.

Authentic, Responsive, and Supportive: We’re just a text away. Trying to build a new company from scratch is a long, difficult, and often lonely journey. We think the least investors can do is be authentic, responsive, and supportive throughout the ups and downs of building a startup.

Over time we’ll expand these capabilities, but our north star will remain earning a high NPS score with the founders we back. I wasn’t going to include any founder testimonials, but Craig at Dwelling shared this when I showed him a draft of this post last night:

More on Fund 2

Here’s some of the fine print on Banana Fund 2:

Target Fund Size: $20 million

Investment Period: 24 to 30 months

Capital Calls: 25% in each of four separate calls*

Management Fee: 1.6% blended

Carried Interest: 20% (30% at 5x performance target)

Fund Formation: Cooley

Fund Admin & Back Office: AngelList

Other: Quarterly LP updates, annual audited financial statements

*I believe AngelList requires the full amount to be wired upfront under a certain check size.

We’re lucky to have many of the same investors backing us again. Despite the current market, our Fund 2 first close had 83% total dollar retention on existing institutional investors from Fund 1. But we wanted to include even more LPs in Fund 2.

Generally, the standard venture capital fund has a 506(b) designation, which means the firm can’t mention the fundraise publicly under Regulation D. We’re closing out Fund 2 with a 506(c) designation which means, amongst other things, we can share details publicly and give more people the opportunity to participate. And using AngelList as our fund administrator makes the 506(c) process simple and straightforward for both us and LPs (if you're a fund manager, check it out for yourself here).

We’re being strategic in putting together the rest of Fund 2 and we can’t guarantee we’ll be able to fit everyone in. The biggest limitation to this approach is that most investors in a 506(c) fund must be a Qualified Purchaser. With this in mind, we’ll prioritize groups traditionally underrepresented on fund cap tables, long-time readers (of The Split, my old blog, and my Twitter), investors that bring unique capabilities and perspectives to the fund, and larger check sizes. Please share this with someone you think might be a good fit! 🙏

If you’re interested in joining us in Banana Fund 2, indicate your interest here.

I’ll follow up within 24 hours and we can share more materials. For commitments of $50,000 or more, we can jump on a call to answer more questions.

I’ll keep everyone updated as we close out Banana Fund 2. See below for the fine print, and back to our regularly scheduled programming on Thursday!

And now, all the fine print:

This is not investment advice. Investing in venture capital funds is inherently risky and illiquid. It involves a high degree of risk and is suitable only for sophisticated and qualified investors. Past performance is not indicative of future returns. Information on this page is qualified in its entirety by the Limited Partnership Agreement, Private Placement Memorandum, and Subscription Agreement, which should be reviewed carefully prior to making an investment decision. Before making an investment, review these documents for full details regarding risks, minimum investment, fees and expenses which will be provided to those invited to invest. The fund uses AngelList Venture (“AngelList”) to provide many of its back office services.

All returns are unrealized. Valuations are calculated as of September 30th, 2022 and have not been audited. Underlying IRR calculation uses the actual dates when investments were made and may include uninvested cash. It measures the asset-level returns of each of the funds' investments, calculated net of fees and carried interest charged by the AngelList platform or the fund manager. The timing and magnitude of fund cash flows are integral to IRR performance calculations, and a small number of investments have a material impact on IRRs. IRR calculations are also significantly impacted by valuations and discount rate assumptions, which are inherently discretionary.

For purposes of calculating unrealized returns, companies are valued with industry-standard methods. For more information on AngelList’s valuation methodology, please see here.

Interesting approach to building Fund 2 — especially the focus on early-stage global investments and keeping things transparent while raising publicly. The structure and strategy seem well thought out, especially with check sizes around $500k–$1M and a $20M target fund https://rentyachtsthai.com/

It's a long, challenging, and frequently isolating experience to try to start a new business from scratch. We believe that being genuine, receptive, and encouraging during the highs and lows of starting a business is the least that investors can do. https://driftbossgame.io