A Deep Dive on Snap's Content Business, Augmented Reality Plans, and Valuation [Originally published April 26th, 2018]

I originally published this here on Seeking Alpha on April 26th, 2018.

Summary

The fear of users leaving Snapchat is overdone. Snapchat’s engaged network of camera messaging users is very sticky – and of comparable size to Facebook in the largest ad markets.

Snap transitioned ~90% of its Snap Ad business to a self-serve ad platform in 2017. Prices dropped 70% YoY (which have now stabilized) masking a 575% growth in ad impressions.

Discover, Snapchat’s premium content product, has higher ad prices and inventory than Stories. Comments by management and Discover Publishers indicate increased usage post-redesign.

Better monetization of Snap Shows and the new Discover Feed ads could contribute $3B in annualized revenue within a few years, falling to the bottom-line and increasing Snap’s margins.

Snap is positioning Snapchat as a cross-device Augmented Reality ecosystem for both consumers and developers, a market that could reach $90B as soon as 2022.

Introduction

Back in December, I wrote about how the Snapchat redesign would affect the stock. After beating Q4 ’17 earnings expectations, Snap’s stock has pulled back considerably as over 1.25 million users and multiple celebrities spoke out against the redesign. Stepping back and looking at big picture, Facebook saw similar backlash when it first introduced the news feed in 2006, a product that brought in nearly $40 billion in revenue between Facebook and Instagram in 2017. User’s main concern with the redesign was that it was too hard to see stories from friends, which the newest Snapchat beta seems to already address.

The most outspoken against the redesign – teens – have continued to show their loyalty to the app. The Spring 2018 edition of Piper Jaffray’s bi-annual Taking Stock with Teens survey reported that Snapchat was the favorite social media platform of 45% of teens in the US, down only 2% from 47% in the Fall 2017 survey despite the flurry of backlash following the February redesign. It also seems few of those users permanently left, as 83% of respondents used the app, versus 82% in the survey six months prior.

The decrease in Snapchat usage post-redesign seems to be relatively mild. A note from Stifel mentioned that Snap’s total audience size (roughly equates to MAU’s or Monthly Active Users) in the US, Canada, and the UK decreased 0.1%, 1.1%, and 1.1%, respectively between January and February. The chart below shows a similar story from ComScore data, which also showed an uptick in March.

Losing users is nothing new for Snap. Its user base has declined multiple times in the last four years (see chart above), and Snapchat’s US MAU’s actually declined 20% between May and September of 2014. Snap reports quarterly DAU’s (Daily Active Users) as an average over the entire quarter, different than competitors who report as of the last month in the quarter. Taking into account the large jump in MAU’s in December, Snap’s Q1 average US MAU’s appear to be approximately 5 million higher than Q4. Even at a 50% rate, US DAU’s increasing 2.5 million match Stifel’s projected global Q1 user growth.

Snapchat Redesign Appears to Benefit Publishers

Early metrics for the redesign appear favorable for publishers, and show how Snap has lessened its reliance on the sort of influencers that have spoken out against the redesign. When testing the new design before rolling out to all US users, Snap saw a 40% increase in users watching Publisher stories in the new Discover Feed. For all the anecdotal evidence that Discover views are plummeting post-redesign, there’s cases like NBC, which recently said that its twice-daily Snapchat Show, Stay Tuned, is on pace to reach 37-38 million unique viewers in March, up 12-15% from 33 million in February and an estimated 28 million in January (up 32-35%). NBC disclosed more than half of those viewers watched the show at least three times in the past week as of March 14th, a number NBC says is also increasing. Self reportedly just saw its best month ever on Snapchat, with a 14% increase in daily viewers over January and 10 million unique visitors in February, up from a historical average of 8 million. And Teen Vogue recently reported a 525% increase in unique viewers March.

Snapchat’s Competitive Advantage is its Messaging Network

A common misconception is that Snapchat’s business has no barriers to entry – anyone can create a camera-based app with disappearing messages! That’s true, and Facebook did – four times (Poke, Slingshot, Bolt, and now Direct). An overlooked aspect of Snapchat that keeps users coming back despite heavy competition is its “Snap Streaks” feature; a unique form of social currency that displays how many consecutive days a user has messaged each friend. Another is Memories, which allows users to bypass their phones camera roll and privately save their photos directly to their Snapchat account. It could be argued that many users treat Snapchat Memories as a secondary, or even primary camera roll, as Snap recently disclosed that each day, more than one-third of active Snapchat users swipe into the Memories feature and tens of millions more users are saving Snaps to their Memories. Snapchat also allows users to create stickers from a snap, saved to their account to be used again forever. These features, amongst others, have created lock-in that has kept users coming back to Snapchat daily.

The true power in Snapchat’s messaging network is not in saving content, however – it is in creating and sending it. Since Instagram Stories was launched in August of 2016, the number of Snaps (a picture or video message) created per day increased from 2.5B in Q3 ’16 to 3.5B in Q3 ‘17, a 40% year-over-year increase.

Source: Snap Q3 '17 Earnings Presentation

3.5 billion per day is 1.27 trillion per year, greater than the estimated 1.2 trillion digital photos to be taken in 2017 in the entire world, excluding Snapchat. So much content is created on Snapchat because it is a private messaging network. There is no pressure for user’s content to receive a certain number of likes or comments, and there is no history – a user is not defined by their profile, and their snaps represent their true, current self. The only form of social currency on Snapchat – streaks – shows consecutive days snaps have been sent back and forth between friends, building a sense of connection and friendship while using Snapchat’s camera.

The high frequency of content creation is very important, especially when it comes to messaging, as each message pushes a notification that pulls another user into the Snapchat ecosystem. This pulling mechanism gets stronger as more users create and send each other content on the platform – a much different dynamic than simply uploading to a story or posting to a news feed, which remains the primary use cases of Snapchat’s oft cited rivals Facebook and Instagram. Not only are Facebook’s longstanding issues that have recently came to light much more serious, continuing to get worse, and more damaging for employee morale than Snap’s (not to mention US consumers are trusting and using Facebook less), but investors must also realize that Facebook and Snap have very different business models.

Facebook’s News Feed is So Successful That It Never Monetized Content

Facebook’s failed Snapchat clones all had great functionality, but they lacked what Snapchat had – a network of messaging users. Facebook’s Stories features have had slightly more success that its messaging clones, with Instagram Stories, WhatsApp, and Messenger Day having 300 million, 300 million, and 70 million daily users of the Stories features, respectively. However Facebook has given zero geographical breakdown of where these Stories users are located. And Facebook has an abundance of users in small advertising markets (more on that later), such as WhatsApp’s reported 200 million MAU’s in India, which appears to make up the majority of WhatsApp Stories users, most of which are uploading images from their camera roll and not using the in-app camera.

In addition to not providing a geographical breakdown of Stories users, Facebook also gives no indication on how many users are actually creating versus simply viewing the stories of celebrities, influencers, brands, etc. Snap discloses over 60% of DAU’s (112 million) create with its camera every day. Instagram has disclosed that 95 million photos and videos were uploadedper day as recently as June of 2016, but any mention of this has been removed from all public materials since Snap first disclosed its “snaps created per day” metric in its S-1 filing to go public.

An often overlooked aspect to Facebook’s business model is that it has always struggled to make money from users consuming content. Instant Articles failed to catch on as more than half of its partners have abandoned the feature. Facebook recently introduced pre-roll ads to Watch, its YouTube competitor, but it has historically struggled to get pre-roll ads to perform well in a feed (it doesn’t help that most users simply hate pre-roll ads in general).

On Facebook’s struggles with monetizing content with pre-roll video ads, Zuckerberg himself said: "We don't need to do pre-roll because our model is not one where you come to Facebook to watch one piece of content, you come to look at a feed". Facebook COO Sheryl Sandberg has also stated something similar: Facebook is not a media company. Instagram’s decision to clone Stories also reportedly came from Zuckerberg himself. It was initially resisted by Instagram’s management team, further suggesting that Instagram’s in-app camera is truly less of a strategic priority than its feed.

Facebook has always struggled to monetize content because its business model never incentivized it to value quality content. Facebook and Snapchat have historically reported similar numbers of “video views” on their platforms; however a stark difference between the two is that video views on Snapchat have always been deliberate, whereas the majority of videos played on Facebook are watched while scrolling. Facebook generates nearly all of its revenue from users scrolling through the news feeds on Facebook and Instagram, via sponsored ads and page owners boosting their posts in the feed. Interacting with content in the feed does provide data to Facebook’s algorithm, but that has historically been the extent of Facebook’s relationship with content. Theoretically, Facebook actually does not want users to spend time actually consuming content, as it means less time training the algorithm and scrolling the feed and viewing ads. This system has worked very well historically thanks to a combination of rising ad prices (or CPM’s – cost per thousand views. A CPM of $10 is $0.01 per view), and increased ad impressions due to a higher frequency of ads and more time spent scrolling.

Contrary to Facebook, Snap’s business model incentivizes users to actually view content, not just scroll. Since Snap has always shared revenue with publishers, which incentivized both Snap and its content partners to create quality, engaging content. And by opening directly to the camera, Snap also has a built-in advantage in AR, which is experienced in a camera, not a feed. Understanding the fundamental difference in business models helps investors realize how completely different the two companies are.

Snapchat Has a Unique Video Content and Advertising Product That Maximizes Video Ad Inventory

The media has heralded Facebook’s “success” in stories, however the graphic below taken from Snap’s S-1 illustrates the strength of Snapchat’s unique content strategy: the Live Stories and Publisher Stories that are unique to Snapchat’s Discover section serve a much higher ad load than user submitted stories. Ultimately, the value that Stories has over a feed is the ability to create video ad inventory out of every piece of content. Considering that as ads are not shown after every user story, and user stories (specifically influencers that skew heavily towards Instagram) may be up to 10 minutes long, Snapchat’s unique publisher content is much more monetizable than user submitted stories (and higher value than competitor Facebook Messenger’s sponsored text messages). And it’s no coincidence. From the beginning, Snap CEO Evan Spiegel viewed advertising as a product, not a necessary evil.

Time spent on smartphones is very fragmented, and Discover’s bite-sized, full screen, exclusive, premium made-for-mobile vertical content is more suited for mobile than traditional long-form content. Big brand advertisers have always preferred premium content, and Discover helped solve a supply chain problem for digital advertisers that still exists three years later. Advertisers, publishers, and users love Snap Ads because both Snap and publishers are incentivized for users to view content, the ads are full-screen, two thirds of users view ads with sound, and they are not obtrusive like a typical mid-roll ad, as the “tap to skip” model Snapchat pioneered gives users control of the viewing experience. This leads to a much more engaging ad than “viewing while scrolling feed”. Many times, the Snap Ads blend in with the content, as seen with the ad at 0:14 here. Professional media companies are also bound by contracts and stickier than social media influencers – a lesson Vine learned the hard way (and Instagram and YouTube will learn eventually).

Source: Snapchat Users and Perception of Ads

Stories has recently become a popular product outside of Snapchat, and it is inevitable Facebook eventually places ads within long influencer stories and tweaks the Facebook and Instagram news feeds to go video-first, looking similar to Snapchat’s new Discover Feed (amid similar levels of user backlash). But Facebook and Instagram are still at their cores designed around a feed model that was optimized for text on desktop. And while Facebook has no debt on its balance sheet, its users have extreme behavioral debt to the feed, something that Facebook has historically been unable to repay when it comes to building a business around the camera or full screen video ads.

The efforts and design of Watch, Facebook’s dedicated video tab launched in August of 2017, tell us that a mobile-only platform that actually competes with Discover is not its goal – It wants to eventually get into consumers TV sets. Early reports, however, show users prefer scrolling the feed over the Watch tab. CBS tested the audience of Facebook’s Watch section by not promoting the shows within the news feed, and the audience “was in the hundreds or single-digit thousands of views — it was literally nothing".

Watch monetization also appears to be terrible for publishers. Per Digiday, publishers in Watch see CPM’s as low as $0.15 to $0.75 when considering that very few viewers stick through the mid-roll ads. On March 1st, Digiday reported CPM’s on ads in Snapchat Shows appear be in the $6-10 range when booked through Snap (with a 50/50 revenue share), and $15-20 for sales booked by publishers (of which Facebook has historically not allowed) with a 70/30 share. All-in, the $3-14 CPM’s received by publishers on Snapchat are nearly twenty times higher than on Watch, with even higher overall monetization when considering the much higher view counts, frequency of ads, and completion rates on Discover convent compared to Watch.

Snap has many other competitors in the vertical news and content space: AMP Stories by Google (off to a slow start), Twitter Moments, Flipboard, and Sip by Product Hunt to name a few. And the goal for all these companies is simple: create digital video ad inventory in a way that can affectively target users at scale. Ultimately, Discover does well because of its large, relevant, and engaged audience in the US and Europe, and because it prioritized monetization and profitability for its media partners from the very beginning (similar to China’s Toutiaou). Snapchat may be slowly evolving into a content destination, but Snapchat is ultimately a messaging app, and it will look to play off that strength to continue evolving in to new lines of business.

How did a Messaging App Get into the Content Business?

Snapchat leveraged its network of users messaging with the camera to gradually position itself in content. Its first evolution away from messaging, Stories, was successful because adding to your story was frictionless; it took minimal effort if you were already snapping your friends. Stories were an important first step for Snap, because as Stories gained in popularity, it slowly trained users to head to Snapchat to sit back and passively consume content.

Snapchat then “laddered up” from stories to create Live Stories. Snap hired editors and used location-based technology to curate user submitted snaps into a custom story, which gave viewers a wide range of authentic perspectives on what was going on around the world in real-time. These were novel at first, and have slowly increased in number and applicability over time to include sporting events, concerts, political debates/election coverage, breaking news, and holidays or day-long events like Christmas, Halloween, and the last day of school. Recently, Snapchat featured numerous Live Stories for the 2018 Winter Olympics. As this article highlights, "Snapchat is getting plenty of behind-the-scenes video from Olympic athletes at no cost, as many of them use the platform to communicate with friends and fans." This is a key aspect of Snap’s business model when other video providers spend billions on content every year.

Source: Netflix spends more on content than anyone else on the internet — and many TV networks, too

Snapchat now creates Live Stories for nearly every breaking news event – and its approach of using raw footage directly from the scene of events (after being screened by Snap’s editors) has helped keep it clear of the fake news problem that has put Facebook, Google, and Twitter under the pressure of US and EU lawmakers.

Snap recently allowed Stories to be shared outside of the app and embedded within web pages (just as Twitter did with tweets) and launched a web version of the Snap Map in February. Snap also partnered with Tegna, which owns local TV stations in 39 networks, to use Snapchat content in its TV broadcasts. “Winning” in the breaking news business is nearly impossible in the age of the internet, with nearly every citizen having access to a camera and the ability to broadcast to the world. Large platforms have become essential to sharing news, and Snapchat’s control of the camera of the developed world allows it to participate in users breaking a story, as it has raw location and metadata related to the 3.5 billion snaps taken every day.

From User-Submitted to Professional Content

From Live Stories, Snap laddered into Discover, which offers premium content published by over 80+ media companies. This transition worked well, as Snap leveraged behaviors that users learned from passively consuming Stories to get them watching Discover. If Snap would have introduced Discover before Stories, it may not have caught on – not only with users, but also with both advertisers and publishers.

This switch to passive viewing was important for Snap, as passive viewers are much more conductive to being shown and retaining ads, and Discover content has a much higher ad load (and ad pricing) than stories. It was also very important because it gave Snapchat stickiness beyond just messaging: If Snap could get users to open the app to specifically watch content, it would give Snapchat a similar pull that watching Netflix or traditional TV has when you’re bored. And even with few friends on the app, Discover made sure there was always something to be watched.

Snap has been experimenting with adding smaller publishers to Discover, something that will inevitably accelerate soon. And while it is hard to find screenshots of the publisher platform, I would assume the tool is similar to Snap’s Ad Manager – meaning there are immediate synergies between new features added on both the content and advertising sides. The quality of content put out from the smaller publishers like the Syracuse and Wisconsin school newspapers has increased over the last few months to a level similar to the larger publishers, giving clues that Snap’s editing platform is fairly sophisticated, yet easy enough for a small staff of college newspaper students to use efficiently.

Still, not every user is using Discover. Some may highlight the subpar quality of the content and that Snapchat evidently lost some users because of the redesign. But this Pew Research Center study from August of 2017 shows that 29% of Snapchat users get news from the app (which doubled year-over-year), and 21% of all18-29 year olds in the USnow get their news from Snapchat. If you explore the younger range of the 18-29 year old demographic, or the 13-17 year olds, Snapchat captures significant market share in key younger demographics. This study was also done before the redesign, which appears to have increased Discover usage.

The Next Step: Mobile TV for Millennials and Gen Z

One very unique aspect of Snapchat’s Discover feature at launch was that it matched the ephemeral nature of Snapchat and traditional TV. This went against everything that digital media has come to represent – always available, on-demand content that lasts forever. This short-lived, fleeting nature brought the scarcity model of traditional TV to mobile, helping Snapchat land partnerships with nearly every major US TV network and sporting league. Each brought not only their own content and expertise, but many also introduced their own advertising partners to Snapchat [More info on TV network deals: A&E Networks, BBC, CBS, Discover, Disney (ESPN), Fox, NBC, MGM, Scripps, TBS, Time Warner, Viacom, and Vice].

The struggles of traditional TV are no secret. US consumers continue to cancel cable subscription at an accelerating pace. AdAge reports recent Nielsen measures show there are only two scripted series averaging more than 3 million live, same-day adult viewers aged 18 to 49. Additionally, “nearly 40% of the 78 scripted shows that have aired since the season began are delivering fractional ratings. Put another way, they reach less than 1% of the demo most coveted by TV advertisers.”

Source: REDEF

The pain is most likely temporary, as legacy TV networks will eventually develop their own mobile and smart TV apps for distribution in the transition away from cable. During this time of transition (and probably thereafter), Snapchat has a comparable, if not greater, reach than legacy TV. At the 2017 Edinburgh TV Festival, Snap’s Head of Content Nick Bell, said "some of our hit shows will reach 50 million people per episode in a 24 hour period".

The graphic below details the estimated reach of a few Snap Shows in January of 2018. As referenced above, NBC’s Stay Tune’s monthly reach has increased to 37-38 million after the February re-design. Stay Tuned averages 2.5 million viewers per twice-daily episode; and ESPN’s Sports Center twice-daily episodes reach 1.8 million to 2 million views per episode (75% of which are between the ages of 13 and 24), often reaching a larger audience than the 6pm version of SportsCenter on linear TV.

Source: Snapchat is enlisting more publishers to make video shows

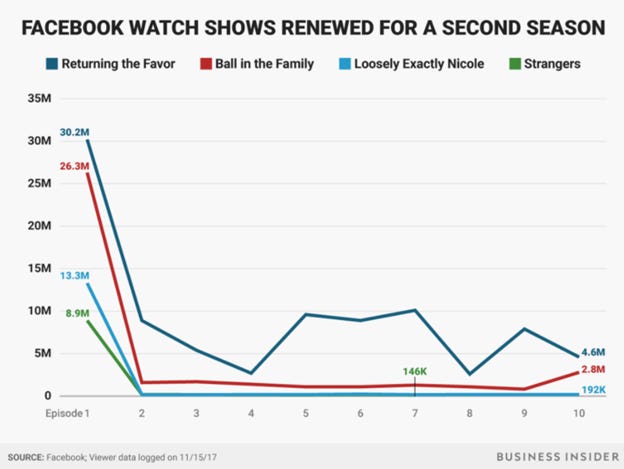

A few more Snap Show and Live Stories viewership numbers can be seen below.

Source: Here's why Snapchat is a valuable partner for TV networks

It could be argued that it’s easier to get someone to watch a four minute show on Snapchat than a live 30 minute broadcast on traditional TV. According to Travis Howe, ESPN SVP of Digital Ad Product and Sales Strategy, "Yes, but that's how people consume content on Snap. Arguably, you may not get someone to watch a two minute show on television because by the time they've tuned in they've missed it. So it is a completely relevant statistic for the viewing behaviors on Snap."

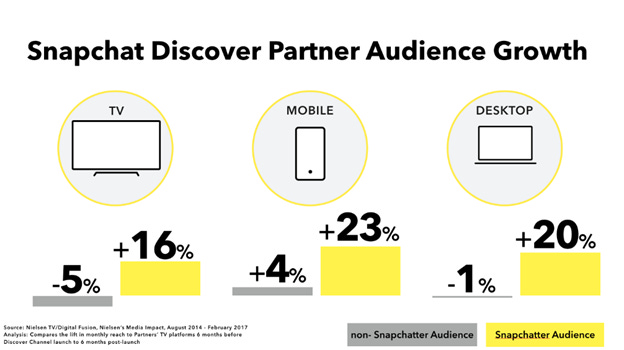

Since Snap launched Discover, it has been extremely valuable for its partners. According to this study from Nielsen, a presence on Snapchat actually boosts its Discover partner’s viewership on traditional TV, the web, and mobile.

The partnerships have benefited Snap as well: Many of Snap’s Discover partners brought over new advertising relationships that would not have otherwise tried (and stuck with) Snap’s ad products. The professional content also minimizes influencer risk, and users will come back to watch their favorite Shows that are contractually obligated to be shown in the app. Snap also has nearly zero marketing cost for its content as its partners are financially incentivized to drive traffic from outside the app.

Data is Important; Both in Ad Targeting AND Content Creation

Beyond reaching a large audience, Snapchat provides advertisers something they do not get on traditional TV – targeting. While Snapchat does not have the same granular targeting capabilities as Facebook, it has quietly beefed up its targeting and measurement capabilities within the past year and a half, borrowing many features from Facebook. These include behavioral targeting, targeting users who previously interacted with an advertiser in the app, Audience Match and Lookalikes, linking offline purchases to Snap Ads, and its unique Snap to Store product (acquiring Placed in June of 2017), which measures if Snap Ads incentivized a user to visit the advertisers physical store. It has over 450 pre-defined targeting audiences, as well as recently expanded location targeting options.

It seems unlikely Snap will ever be able to create the sort of user data profiles like Facebook that would allow an advertiser to specifically target “Republican cat owners with diabetes” or even “interest in illegal firearms”; but if an advertiser can target new parents in Chicago, as this marketer does here, it offers a compelling opportunity – and for traditional big brand advertisers on the AdAge Top 100, who spent over $267 billion in 2016, it is superior to “someone who may be in the room, and may or may not be paying attention to the TV, while this commercial is airing on ESPN”.

Snap’s approach to content also gives it control over how it builds targeting inputs. On any given day, Discover includes content ranging from food and cooking, political or cultural events, nearly every major professional sport, fashion and beauty, comedy, video gaming, auto racing and cars, etc. Snap can develop new Discover content to create custom audiences based on specific interests.

And this data created through Snap’s content business is not just for ad targeting – Snap reportedly studies and shares detailed data on how content is viewed with its Discover partners, aiding in the production of future content. And in the time it takes a user to create one data point watching a traditional 30 minute TV episode, Snap gathers 10 from its three minute episodes.

Due to the short length and relatively low production quality of Snap Shows, Snap’s content costs are also theoretically very low compared to traditional TV networks, ranging from $6k-$45k per episode. Meanwhile, traditional long-form content with high production values cost anywhere from $1-$10 millionper episode, with everyone from Netflix, Hulu, HBO, Apple, YouTube, Facebook, Verizon, among others, all bidding up content prices competing in the new world of streaming libraries that can generate revenue over extremely long periods of time. Paying as little as $6k per episode, Snap can afford risky bets on Shows that do not pay-off. At that cost, Snap could theoretically fund 1,667 episodes at the same price as a $10M long-form TV episode.

Amazon, which just disclosed Prime Video had a US audience of about 26 million, just committed to spending $1B to develop a five season Lord of the Rings series. Facebook has joined the party too, paying a range of $550k-$750k per episode for Watch content. Facebook also recently bought the rights to LaVar Ball’s, “Ball in the Family”, for roughly $30k-$40k per minute. Early Watch results, however, seem to be poor, with views plummeting after the first episodes.

Ultimately, just like how consumers watch many different channels within a cable package, consumers will subscribe to, and watch content from, multiple providers. The shorter, cheaper, and more varied the content is, the more valuable it will become for content distribution platforms that sell targeted ads. Snap seems to have a structural advantage due to the way it built its low cost content business.

Snap Shows Have Significant Revenue Upside

Beyond the increased publisher views brought on by the redesign, Snap Shows have immediate upside. Snap originally booked Snap Show ads at fixed pricing, ranging from $0.02 per impression with a 50/50 revenue share with the publisher, to up front sponsorships like Match.com did with Hungry Hearts. Per Digiday, Snap was slow to book fixed-rate deals in its Shows until at least the end of October, with three of the six Snap Showsfeatured on Oct 20th 2017 showingzero ads; making it no coincidence Snap missed revenue projections its first three quarters as a public company.

Due to the slow start, revenue from Snap Shows was relatively muted in 2017. Digiday reportedSnap began filling un-booked Snap Shows ad slots with its self-serve programmatic platform mid-way through Q4, which was also its first quarterly revenue beat as a public company. CPM’s on Snap Sold inventory is reportedly in the $6-10 CPM range, while Partner Sold comes in around $15-20. All told, recent programmatic ads are selling for about half the rate of fixed pricing – but much better than showing no ads at all – and at nearly zero marginal cost as the content would have been viewed regardless.

Using a conservative $5 CPM for every single Snap Show, assuming Snap has a 50% revenue share on every show, and Snap’s typical three ads per show, Snap would make just less than one cent per view ($0.0075). Assuming an average of 6 million views per show (based on some of the numbers above), on its goal of 5 shows per day (on about 80 different show series per year), projects annualized revenue of $82 million at $225k per day.

I personally think these estimates are too conservative, as there is a lot of upside in Snap Shows from 1) increasing CPM’s, 2) increasing the views on each episode, 3) optimizing the mix of ads in each show, 4) increasing the number of new episodes per day, 5) licensing content for a fixed cost and keeping all revenue, 6) product/sponsored placement within shows, and even 7) distributing Shows or content IP on other platforms.

Snap has stated on nearly every conference call since going public that advertisers adopted its self-serve ad platform quicker than expected, which depressed CPM’s by nearly 70% YoY in Q4 to the $6-10 range. Prices will increase as more advertisers realize the high ROI of Snap Ads at current prices and enter the auction. Advertisers are also more likely to sponsor entire seasons (at higher or fixed prices) after Snap has proven consistent viewership and starts rolling out second and third seasons in 2018. Snap is also beginning to allow Discover partners to run branded ads that blend in with their content, which hints at more fixed pricing. As traditional TV networks reduce ad load in live programming to compete with uninterrupted online streaming, it also is likely CPM’s for live broadcasts rise, making Snap Ads look more affordable comparatively.

Increasing the number of views on each show is also low hanging fruit, as the new Discover Feed allows Snap to source literally any piece of content (not just Shows, but publisher or influencer stories as well). Before the redesign, episodes disappeared from Discover after 48 hours, and only some series could be found by crafty users using Snap Search. Now, Shows can be sourced in the Feed weeks or months after release. If a user watches an episode of the Food Network’s Chopped show, Snap can populate the feed with other episodes in the series. It can also put a user’s favorite show at the top of the feed – something that was less likely to grab users’ attention when stories from friends took priority over Publishers in the old Discover design. Snap also has the option to broadcast shows globally, or even on other platforms (web, mobile, theaters, streaming, etc.), significantly boosting the reach and amortizing the cost per show over a higher revenue base.

Snap could also increase the number of ads per show. Snap appears to be testing ad placement between each auto-advance in Discover content, squeezing in an additional ad on each view (which may have no revenue share). Snap could continue experimenting with length and ad mix in Shows, inserting additional non-intrusive tap-to-skip ads.

Snap can also increase the frequency of new episodes. Comments by management early in 2017 mentioned three shows per day, a number that has since moved up to five. If Snap Shows continue to see success, there is no reason to stop at five per day – especially when they are so inexpensive at $6-45k per episode.

Assuming that CPM’s on Snap Shows eventually reach $20 (in-line with the low-end of traditional TV and high-end of digital video), Snap is able to improve average ad mix to four per show, all Snap Show revenue is still impacted by the 50% revenue share, average viewers per episode double to 12 million, and new episodes per day bumps up to 10, Snap would generate approximately $1.75 billion in annualized Snap Show revenue. At about $4.8 million per day, Snap shows become a 90% gross margin business (not considering hosting costs) if assuming all 10 daily episodes cost near the high end of $45k each.

Snap’s Content Business Cumulates in Live TV Streamed in Snapchat – and Potentially a Platform for Programmatic TV Advertising

Showing investors the next steps in its content business beyond Snap Shows, Snap partnered with NBC to live stream Olympics coverage from within Snapchat. Snap has existing partnerships in place with nearly every traditional TV network, professional sports organization, and its 60-80 media partners on Discover to expand this considerably. Eventually, all these partners (and perhaps select influencers) could launch their own live “channel” within Discover. Twitter’s live streaming strategy is starting to bear fruit, for both itself and its advertising partners. Could Snap do the same?

Live TV on Snapchat also gets interesting when you consider Snap’s Crowd Surf feature launched in the fall of 2017, which uses acoustic fingerprinting technology to link together snaps submitted by different users into one concurrent stream that allows users to jump to different views. Snap could eventually take Spectacles footage and combine multiple angles together to create a seamless live stream of nearly any event. Snap also invested a small amount in autonomous drone startup Skydio, which could mean they are thinking about incorporating third person footage into streams.

Thinking about what the new Discover Feed could look like in a few years when it its live offerings are fully built out, it truly becomes TV for Gen Z. Spiegel has said numerous times that the purpose of Discover was to provide users content while waiting for their friends to reply to a message. Just like consumers used to channel surf pre-Internet, or browse Netflix today, Snapchat has become a content destination to kill time.

Snap currently does not have ad products for “Live TV”, but its entire non-AR ad business is based around full-screen video ads. Ads are currently limited to 10 seconds, but Snap could introduce non-skippable, longer-form ads into its self-serve ad manager if it goes the way of live TV. Snap may also forgo doing the advertising internally, and partners could just pay Snap to broadcast their own stream that they then monetize themselves.

There is also the possibility for Snap to eventually create a programmatic digital ad platform for its media partners to plug in to their own streaming apps, similar to Google’s DoubeClick for digital publishers. Disney’s contract with FreeWheel actually expires soon, and among both Google (which powers CBS All Access app) and Comcast, there is speculation that Disney may work with a smaller player to avoid working with Google or Comcast.

Snap acquired MetaMarkets in 2017, which offered live inventory discovery and bid monitoring, gave clients an API to import data into other apps, and aggregated ad metrics over numerous ad platforms. This acquisition tells us Snap may be looking to incorporate multiple third party programmatic campaigns, from numerous advertising exchanges, into its own ad manager. This would not put it in competition with FreeWheel, but more so a tool for advertisers and content partners to better measure and coordinate their entire ad campaigns across multiple platforms.

A network like NBC has the capital to create a wide enough variety of content to create targeted user profiles (and has its own product in Comcast’s FreeWheel), however a targeting option like “goes to the beach” is hard for even Comcast to deduct based on streaming activity that is generally done on WiFi. Some of the smaller Discover partners or more niche TV networks would benefit from being able to tap into Snap’s massive user profiles on nearly one hundred million Americans, either in their own apps or within Snapchat’s Live TV offering. Snap benefits from these partnerships as well, as new types of content within Snapchat or on its partners services provide additional viewer data that can be used in both targeting and future content creation as mentioned above.

The New Discover Feed Introduces Native Feed Ads and Boosts Content Views

On Black Friday, Snap announced its newest ad product, Promoted Stories. Thinking about this ad format in the context of the new Discover Feed, it fits into Snap’s advertising offerings similar to a native news feed ad on Facebook or Instagram, a product that brought in nearly $40 billion in revenue between Facebook and Instagram in 2017.

Source: Author’s screenshot of the new Snapchat redesign showing a Sponsored Story appearing in the Discover Feed when first swiping to the feed (left) and after scrolling down (right).

At launch, Marketing Land reported Sponsored Stories would sell fixed rate, single-day countrywide takeovers, with metrics on impressions in the feed, how many users tapped on the story, how many watched until the end, and the effective cost of all those metrics based on the price. AdAge also reported that they are expected to evolve into a targeted ad product served through Snap’s self-serve platform based on impressions. Not only does this give Snap a product that digital marketers are extremely familiar with due to Facebook’s success, it also creates an opportunity for advertisers to recycle the videos created for Sponsored Stories as Snap Ads within Discover content.

The new Discover Feed also changes the game for Snap Shows and Publisher Stories. In Snapchat’s old Discover design, posts from friends and influencers were featured much more prominently than Snap Shows or Publisher stories. The new Discover Feed seems to put more emphasis on Shows and Publisher Stories – two products that are much more profitable for Snap than stories from friends and influencers. If Snap figures out that a user likes a particular Snap Show, it can serve them subsequent episodes in the season; essentially allowing users to binge watch Snap Shows as they could on Netflix. Snapchat will be able to provide users an endless stream of content, whether it was created one hour ago or one week ago. Discover also now auto-plays to the next item (prior it returned to the Discover section), occasionally inserting ads in between each auto play. Content in Discover is now displayed in-app in a more pleasing vertical orientation, no longer crammed in horizontal bars underneath friend’s stories as it was in the old design. The Feed also sources stories from influencers that users do not follow, helping them grow their audience – a common complaint of Snapchat, and a reason influencers eventually embraced Instagram Stories.

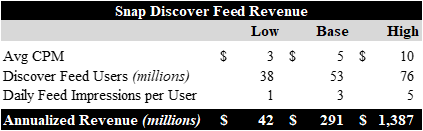

Thinking about the Discover Feed from a financial perspective, we can start with assuming the 38 million daily Discover viewers as of the summer of 2017 as leaked per the Daily Beast, see one ad feed impression per day. At a conservative $3 CPM, it’s an additional $42 million in annual revenue. Playing around with the numbers, assuming the 38 million users increases by the 40% Snap saw in early tests of the redesign, the number of impressions jumps to 5 per day, and the Discover feed sees CPM’s similar to Facebook’s news feed, revenue could be $1.4 billion or more in a few years. And the revenue may entirely fall to the bottom line, as there is a very low marginal hosting cost in putting an ad in the Discover section that users have already been scrolling through and incurring hosting costs since 2015. Screenshots have recently surfaced of Snapchat testing old versions of the Discover section, but the point remains that feed revenue stands to be a significant revenue driver going forward.

Snapchat Continues to Reach a Large, Unique Audience

Beyond having a unique advertising product, Snap has a large, exclusive reach that is being criminally under appreciated. This App Annie report I have referred to in past articles still holds true: Snapchat reaches an exclusive audience within the United States that cannot be reached on other platforms on any given day. And 79% of users are older than 18, debunking the narrative that Snapchat is only useful for reaching teens.

Source: Snapchat & the Power of Putting Data in Context for Marketers & Advertisers

The consensus seems to be that Snap has no scale. However in August of 2017, MarketingLand compared the total reach of Facebook, Instagram’s Feed, Instagram Stories, and Snapchat (excluding users who use only messaging) as reported in each company’s Ad Manager. As shown the charts below and the article linked above, Snapchat actually reaches a larger audience than Facebook’s properties in a few key demographics.

Snapchat Stories reaches a larger audience than Instagram Stories in the US, UK, Canada, Australia, and France. When looking at the 13-17 year old demographic specifically, Snapchat completely dwarves the above markets, including Germany.

Source: How Facebook’s, Instagram’s and Snapchat’s audience size estimates compare

Facebook and Instagram’s huge lead in users comes from very small advertising markets and from the 35+ demographic in the large ones; an important demographic, but one’s who are usually late adopters of new trends, and now starting to move to Snapchat. Instagram also added features in early 2016 that let users easily switch between multiple accounts, contributing to Instagram’s higher user count, yet fewer unique Stories users than Snapchat. Facebook has nearly 700 employees on its internal PR team (plus hundreds working at external PR firms), no doubt a key to its success in distracting advertisers and investors from looking at the details.

Comparing the numbers in the charts above with the (dated, but still relevant) tables below, it becomes clear: Most advertising dollars are spent in markets where Snapchat has a similar reach to Facebook. Zenly, which Snap acquired in the summer of 2017, appears to be fairly popular in three other important and emerging ad markets: Japan, South Korea, and Indonesia.

Source: eMarketer

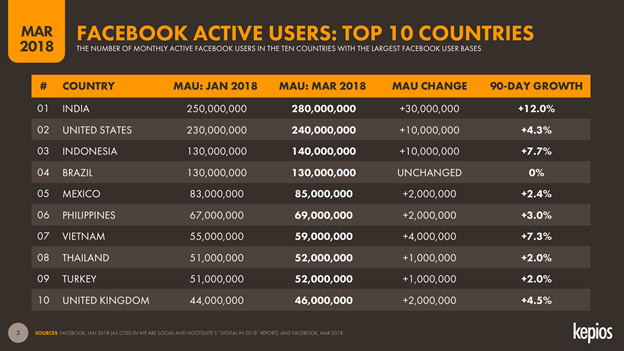

As shown in the image below, Facebook has incredible reach – however most of that reach comes in very small advertising markets. India (280M), Indonesia (140M), Brazil (130M), Mexico (85M), the Phillippines (69M), Vietnam (59M), Thailand (52M), and Turkey (52M) make up 41% of Facebook’s 2,129M MAU’s as of March 2018; however those nine markets were only projected to bring in roughly $6.4B of mobile ad spending in 2018, giving Facebook an upper ARPU range of $7.38 on 41% of its user base if it captures 100% mobile advertising market share.

Source: Data shows you didn’t #DeleteFacebook, so make sure to change these settings

In the five large markets Snap reaches a similar audience to Instagram – the US, the UK, Canada, Australia, and France – mobile ad spend is estimated at $83.4 billion in 2018, 100 times greater than Snap’s 2017 global revenue. Despite Snap’s audience in these five markets being nearly 10% the size of the large Facebook markets mentioned above, the total ad spend in the markets where Snap is competitive is nearly 10x higher.

Unique User Base Positions Snap Favorably for the Next Wave of Computing: Augmented Reality

Beyond just messaging that pulls other users into the app, Snap’s engaged network of users also use the camera to experience Augmented Reality. The AR market is expected to reach $85-90 billion as soon as 2022, with a case to be made it eventually exceeds $1 trillion. Over 95% of that $85-90 billion is expected to come from areas Snap already generates revenue: eCommerce, Hardware, Advertising, Apps/Games, and Location-Based spend. While it is uncertain exactly how AR will evolve over the next few decades, one thing is certain: It must be experienced through the camera.

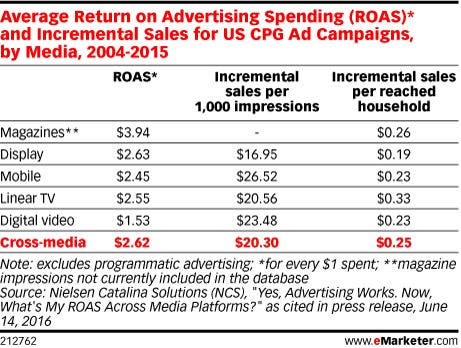

One of the largest, quickest industries to benefit from the camera will be advertising. Lowe’s cites $60B “sitting on the sidelines because customers can’t envision products in their home and don’t pull the trigger on buying”. Forrester estimates only 5% of marketers are using AR now, with 17% planning to use it in 2018 (240% YoY growth), with AR expected to be much more relevant to marketers than VR for the next three years.

A study by the Boston Consulting Group (commissioned by Snap) highlights some early success in AR advertising. Multiple campaigns for consumer goods companies delivered an average 10% increase in sales with a 3.1x return on ad spend, with McDonald’s notably seeing a 10.5x return and significant lift in foot traffic. At current prices, AR RAOS appears to be competitive with other ad mediums. Snap is currently transitioning sponsored lenses from fixed pricing to its self-serve auction platform. Just as CPM’s on Snap Ads declined dramatically in the auction, Snap may be able to do the same with AR advertising – significantly lowering prices to increase returns for advertisers and make it harder for competitors to profitably scale their own AR advertising platforms.

The BCG study reports numerous barriers to increasing AR spend, the largest being a lack of scale. BCG estimates that more than 80 million people in the US, or roughly one-third of all smartphone users, engage with AR at least monthly. Per the report, Snapchat reports 70 million monthly AR users in the US, which would be approximately 87.5% of US AR market share (I think this may be a little high). Snap also has said that half of the entire 13-34 year-old US population plays with AR on Snapchat per week. Globally, a recent Deloitte study projects 300 million consumers will create AR content monthly, and Snap says 70% of its 187 million users (131 million) play with Lenses each month – smaller global market share at 43.7%, but certainly above 50% if you exclude the tens of millions of AR users in China where Snapchat is banned. Certain AR-based apps may rack up fast downloads, however it is unlikely another camera-based platform becomes a daily habit in the same way that Snapchat has, giving it a significant advantage in the distribution of AR to consumers.

Source: Augmented Reality: Is the Camera the Next Big Thing in Advertising?

Snapchat may have less reach than Facebook’s news feed; however AR is experienced with the camera, not in a feed, and Facebook shares very few statistics on how much its in-app cameras are used. Hidden in this recent article, Facebook disclosed to Forbes that more than 1 million users "created video clips" with the Facebook Game of Thrones lens that ran back in August of 2017. Back in August, Variety reported that more than 45 million users "viewed or posted" the Game of Thrones Night King lens that ran on Snapchat during the same time frame. The two day lens campaign for Paddington Bear on Facebook was “used over 26k times” – merely 5% of the lowest daily sponsored lens usage reported in the leaked Snapchat data from between May-September ’17 (Source: page 20).

The second largest barrier to AR advertising is a lack of clarity on ROI. Snap says users are engaged with AR ads for 20 seconds on average – an entirely different dynamic from TV ads, where viewers often change the channel or look away from the screen at their phones. Among the many different targeting features mentioned earlier, Snap just recently introduced a “Shop Now” feature to its AR lenses, a very direct way to measure ROI on Snap’s AR ad products.

Camera advertising also brings back the importance of creativity to advertising, which has slowly fallen to the wayside in the age of hyper targeting (which is at risk of being regulated away). With a lack of solid digital ad options, advertisers put up with Facebook news feed video ads, which auto-play without sound and are actually encouraged by Facebook to have captions – essentially the same as a banner ad from the 90’s.

Other concerns relate to lack of expertise and worries about cost. As I wrote about in December, Snap’s Lens Studio democratizes the AR creation process. It lets anyone from creative professionals to middle school students create AR lenses, and establishes Snapchat as the largest AR distribution platform.

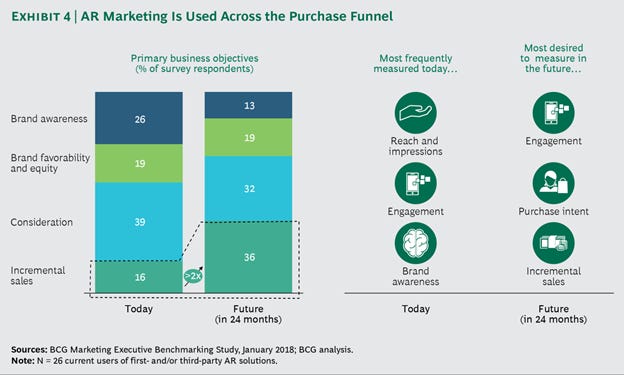

Currently advertisers are looking for reach, impressions, engagement, and brand awareness, areas Snapchat’s AR ads appear to be beating the competition according to marketers. Engagement will remain important in two years, with purchase intent and incremental sales key as well – which Snap has invested in via in-app commerce and offline store visit attribution.

Source: Augmented Reality: Is the Camera the Next Big Thing in Advertising?

Snap Will Use Existing Use Cases to Ladder into Augmented Reality

Looking beyond the advertising that will drive AR revenue growth in the short-term, the end state of AR is contextual computing – data that is overlaid on a 1:1 digital map of the physical world, often referred to as the AR Cloud. This will ultimately be done via cameras in smart glasses that eventually replace smartphones. The AR Cloud will create and reference trillions of digital data points across the entire physical world, potentially indexing the real world similar to how Google search indexes the web. Reaching this point may be over a decade away, and getting there will be a slow, gradual process. Numerous things are holding it back, primarily fitting the tech into fashionable, affordable, and functional smart glasses.

When it comes to Snap’s long-term AR strategy, expect it to draw parallels to its ladder into content. Snap has already leveraged its network of messaging users to introduce Face Filters, 3D World Lenses, and most recently, Context Cards and the Snap Map (all pieces of the puzzle). Due to the complexities of having a digital replica of the entire planet that accurately matches the physical world down to the millimeter, any platform that is able to create a base of both users and developers before releasing AR-enabled smart glasses will have a huge advantage. Apple used the original iPod to build a base of users and train them to download music from iTunes before the launch of the iPhone, which evolved into a cross-platform App Store that now serves numerous Apple products.

Stepping back, Snap is creating an AR ecosystem before launching AR-enabled smartglasses. Snap Lenses are essentially the AR equivalent of apps. And Snap’s Lens Studio, Snap Codes, and Context Cards are tools for developers to begin creating experiences on Snap’s AR ecosystem. Snap will eventually allow developers to monetize their lenses, which will most likely work cross-platform whenever AR-enabled Spectacles launch. Judging by the 131k members in the Snap Lenses subreddit, Snap appears to have generated massive interest in the developer community, most likely due to its scale in distributing AR to consumers.

Gaming will be a big business in AR, especially as consumers increasingly prefer the sort of non-linear, open world gaming experience (Pokemon Go, PUBG, Fortnite, etc) that will work well in AR. Apple’s ARKit has shown the potential of AR gaming apps; and Snap’s Lens Studio will eventually provide the tools for developers to build complex games within Snapchat Lenses. Snap’s mid-2017 acquisition of PlayCanvas, an HTML5 game engine ran entirely in the cloud that allows multiple users to edit at once, indicates Snap is serious about AR/VR gaming. Snap has been running game-based ads and lens games for years now – recently launching a global Easter Egg Hunt via the Snap Map (a hidden asset worthy of its own discussion). On April 25th, Snap introduced Snappables – AR games played with your face that will be a permanent feature in the camera home screen. Other forms of in-app gaming will come next, followed by multiplayer, perhaps laddering from Snap’s new 16 person group video chat feature. Bitmoji, the #1 most downloaded iOS app of 2017 (and another hidden asset worthy of its own discussion), hints at capabilities for developers and users to quickly tap into their own personalized AR (and likely VR) characters. This gives Snap an existing tool to quickly grow in not only AR gaming, but nearly any sort of customized AR, and eventually VR, experience.

Content will eventually be shown in AR, which has been the most difficult piece of AR/VR to solve. Snap has spent years developing its content business, with the recent launch of 3D Bitmoji lenses giving us an idea of how Snap thinks about AR/VR content. Audio and music will eventually blend with AR, and Snap has incorporated music in both face filters and 3D world lenses. AR has use cases in special effects at events and concerts as well, giving Snap opportunities to eventually incorporate distribution of AR-enabled Spectacles at events with its various media partners.

AR has endless commerce purposes too. Snapchat currently has poor conversion metrics (see below) – something that its recent e-commerce initiatives are looking to improve on. Snap has been testing an in-app Snap Store, and will likely ladder existing user behaviors to move further into the space. Snap is building e-commerce functionality within both Discover and Lenses. McDonald’s is rolling out Snap Codes for menu items on trays in France, and Bareburger is using a combination of Snap Codes and Snap Lenses to create restaurant menus that are based entirely in AR, while providing significant cost savings. And Nike recently partnered with Snap for an exclusive launch of the Air Jordan III. Combining Snap’s ability to refer traffic at Facebook-scale (see below) with the fact that Gen Z, the heaviest Snapchat users, contribute to $830 billion in US retail sales annually and convert twice as much on mobile as other demographics (below), Snap seems to be positioned well to compete in e-commerce.

Source: 4 Key Facts You Should Know Before Allocating Ad Spend

The concept we know as Search will also be important in AR. 50% of searches are done locally with many of those done right on the spot of interest. Being able to hold your camera up and get contextual information will certainly save consumers a lot of time – and improve conversions for advertisers if done correctly.

All of these opportunities in AR revolve around the camera – which is why hardware, or smart glasses, appears to be the most competitive in the space. The use cases for smart glasses will be limited at first, most likely revolving around sharing first person content – exactly what Spectacles do now, but will eventually include all the things I’ve mentioned above. Partnerships with nearly every major US sports league gives us a hint of how Spectacles may also play in to Snap’s live streaming feature – the ability to view multiple angles of live, in-game first person footage from players on the ice.

Snap is positioning Snapchat as a mobile/wearable cross-platform product, which will allow Snap to eventually roll-out AR-enabled Spectacles with existing use cases to its network of messaging users. Even if Spectacles never take off, Snap could license its camera operating system to other companies, even auto manufacturers, a similar approach Google took with Android on mobile. Snap partnered with Royal Caribbean to make a Spectacles-powered underwater scuba mask, so they are certainly exploring the idea.

Despite Better Competitive Positioning, Snap Trades at a Significant Discount to Facebook

Using Facebook’s North American ARPU of $82.4 as a benchmark, Snap’s content-heavy monetization strategy appears to have significant room to expand its NA ARPU of $8.7 by over 9x.

As I detailed, Snap could bring in as much as $1.7B and $1.4B in Show and Feed revenue, respectively, over the next few years. Considering Snap’s competitive positioning in AR, it also seems likely Snap wins significant share of the projected $85-90 billion AR market by 2022 – which is not being reflected in the consensus sub-50% revenue growth estimates in 2020 and beyond. Assuming only a 10% share of the AR market ($8.5 billion) and a conservative 25% revenue growth on its current business (which, mind you, increased ad impressions 575% in 2017), Snap could bring in over $13.5 billion in revenue by 2022. This is not doing much to consider the impact of Snap’s eventual Live TV offering, or Bitmoji, the #1 most downloaded iOS app in 2017, and no considerations are being made for the Snap Map, which is quickly becoming a messaging home screen that combines the utility of Yelp and Google Maps (considered one of Google’s most under-monetized assets according to Morgan Stanley’s Brian Nowak).

At the 75% 5-year revenue CAGR to hit $13.5 billion by 2022, Snap trades at a P/S/G of 0.29, a 63% discount to Facebook’s 0.46 based on consensus analyst estimates and a generous 25% 5-year revenue growth rate. AR is likely to still be growing at a rapid rate by 2022, and if it truly does become a trillion dollar market, Snap could be trading a very significant discount to intrinsic value.

As Snap grows, it is unlikely to be valued solely on revenue. A recent leaked internal memo stated Spiegel had a goal for Snap to be profitable in 2018. The market seemed to shrug it off, or at the least assumed it would be done through cost cuts, as Snap recently cut 10% of its engineering staff in February and 100 from its 400 person advertising team at the end of March. What the market seemed to overlook was that Snap implemented a performance evaluation program in 2017, previously having no system for culling underperformers. At the time of writing, Snap had 127 jobs posted on its jobs page, 52 of them in engineering – hardly an indication of drastic cost cutting.

Hidden beneath disappointing top-line numbers, Snap increased Snap Ad impressions by 575% in 2017, and 90% in Q4 alone. This massive increase in impressions was offset by declining CPM’s, down 70% YoY in Q4 ‘17. This occurred due to Snap channeling 90% of Snap Ad revenue through its progmmatic self-serve auction platform, from $0 in Q3 ‘16. The self-serve platform serves as a base for Snap to scale revenue quickly on nearly every future product (AR lenses, Bitmoji advertising, programmatic live TV, and the Snap Map, to name a few), with less friction for customers, and at higher margins than manually placing ad-buys with human sales reps. It also explains Snap laying off some of its advertising team, along with ex-VP of Sales Jeff Lucas.

In Q4, Snap disclosed that over half its revenue was generated outside the AdAge Top 100 advertisers, who spent a combined $267 billion in 2016. Representing less than 0.2% of their budget share, it’s not too farfetched to think Snap has considerable room to grow revenue as the largest marketers look to diversify their digital advertising away from Facebook and Google. Even assuming all $13.5 billion in 2022 revenue comes from big brands, that only represents 5% of their 2016 ad budgets.

CPM’s for Snap’s AR carousel ads are currently priced around $8-20 (with Snap Ads as low as $2.50 in some cases), which is comparable to both premium digital ad prices ($2-6 for display, and $12-20 for video) and traditional TV (anywhere from $14 to $80). The recent Ads.txt study also revealed that online video inventory may be overstated by up to 50 times – with a crackdown potentially boosting CPM’s across the industry.

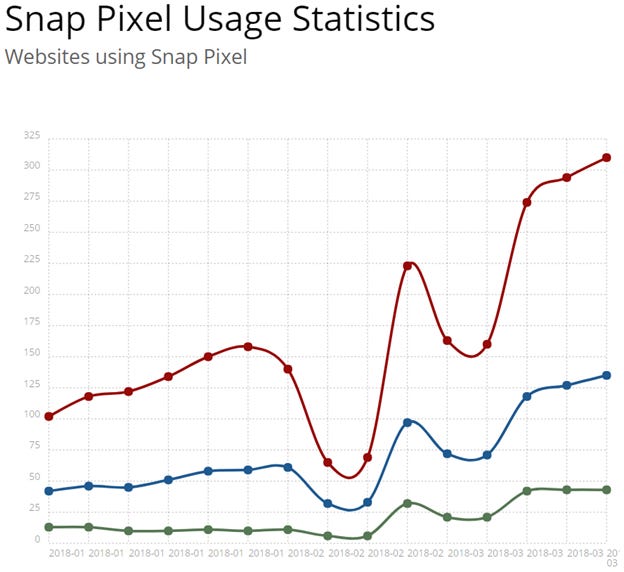

Snap’s CPM’s can only fall so far before marketers notice. Their primary concern with Snap has been its lack of targeting and measurement capabilities, but Snap has invested significantly in targeting (as explained earlier) in first and third party measurement solutions, notably its Pixel tracking tool. In Q4, management stated that one in three Pixel beta partners spent their first dollar on the platform after adopting the pixel, and that contested auctions see ~40% higher CPM’s. The 3x increase in usage of the Pixel over the course of Q1 ’18 appears to indicate more advertisers are joining the auction, contesting and raising CPM’s.

Source: BuiltWith Snap Pixel Usage Statistics

As Snap’s CPM’s stabilize in-line with other digital ad units, revenue in the short-term will be driven by increased ad impressions in Discover, the new Feed, filling empty ad units in Snap Shows, and AR lens carousel ads. These, combined with live TV and impression-based ads on the Snap Map and Bitmoji (article to follow later) will drive medium-term growth, and the economic value created by building out an AR ecosystem will drive long-term growth over the next few decades.

Snap may also continue relying on impression growth to boost supply and drop CPM’s, putting pressure on rivals. Facebook’s management team has repeatedly stated they will rely on rising CPM’s for revenue growth (hard to increase impressions when users spend less time in the app). Facebook’s CPM’s were up 175% YoY (14%, 24%, 35%, and 43% by quarter), with ad load increasing 80% YoY, but decreasing sequentially every quarter (32%, 19%, 10%, and 4%).

Much has been said about Snap’s lack of profitability; however on the Q3 call, CFO Drew Vollero stated that gross margins in the US were over 50%. And when adjusting for non-cash and non-recurring expenses, its reported gross margins has improved in 11 of the last 12 quarters. A central pillar to the Snap bear case is that it won’t be able to grow revenue faster than COGS due to its hosting commitments with Google and Amazon. In Q4 however, Snap increased revenue $77M QoQ, posting 87% contribution margins on its hosting costs, showing that Snap has very low marginal cost on new ad revenue. Snap also said during its roadshow that it expects its cloud hosting costs to actually decline over time as Amazon and Google compete on cost. Google Cloud continues expanding internationally, recently launching a data center in Mumbai, which should also help lower hosting costs related to Snap’s historically more expensive international user base.

The majority of Snap’s operating costs are related to employee salaries and stock-based compensation, and management has repeatedly stated they expect hiring to slow going forward. Much of the areas Snap is adding revenue in 2018 – Snap Shows, Discover Feed ads, and AR lenses – are already being used by users and have large numbers of employees supporting them, yet have been un-monetized. Considering the new self-serve ad platform requires minimal internal support for each additional sale, Snap should have very low marginal costs and it’s very likely that additional revenue falls to the bottom line as the business scales.

Understanding that Snap likely becomes profitable as it scales, looking forward at our prior estimated $13.5 billion in 2022 revenue, at a 20% free cash flow margin (Facebook posted 43% in 2017), free cash flow in 2022 comes in at $2.7 billion. Discounted back to today at a conservative 20% discount rate, Snap trades at a 16.5x FCF multiple, a ~62% discount to FB’s 26.5x.

Conclusion

Even using relatively conservative assumptions, Snap currently trades at a significant discount to Facebook. Snap’s business is evolving into a combination of old school television and new school tech. A mix of messaging, content, advertising, software, and hardware in a way that combines select pieces of WeChat, Viacom, Google, and Apple. Time will tell if Snap truly becomes a major player in these spaces, but it appears to be positioning itself to do just that. The transition to a self-serve ad platform that dampened revenue growth in 2017 appears to be in the past, which will serve as a foundation for Snap to grow the business from a position of strength going forward.